Kevin Warsh officially became Federal Reserve Chair on May 22. In his first Federal Open Market Committee (FOMC) meeting and press conference last week, he signaled a clear break from recent practice. Warsh's comments focused on practical changes at the Fed rather than dramatic shifts in interest-rate policy itself.

Shorter Statements, Less Guidance

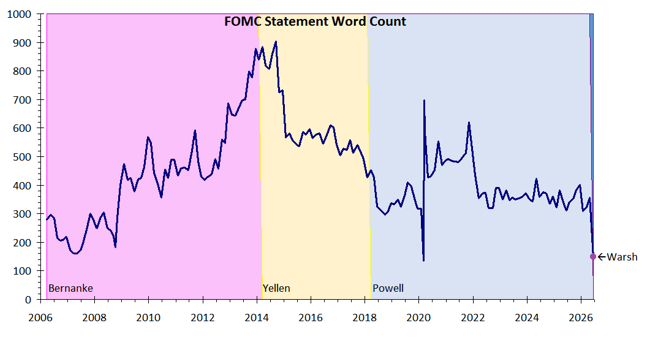

The June FOMC statement was just 147 words in length, down sharply from the roughly 380-word average of the past five years under former Chair Jerome Powell. Chair Warsh stripped away much of the open-ended language in previous statements. Forward guidance was effectively removed, and at the press conference, he declined to answer questions that could be interpreted as signaling future policy moves. He quoted his onetime boss, the late former Treasury Secretary George Shultz: "Press conferences are useful, but be sure you have something to say."

The Summary of Economic Projections (SEP), including the famous "dot plot" of the 19 individual policymakers who contribute to the rate forecasts, will continue, but Warsh said he personally will not contribute to the dots. It appears the Fed is going with a "less is more" approach to its communications. Warsh has said it is better for markets to respond to economic data than to trade on expectations of future Fed actions. Markets may need time to adjust to this new communication approach, which could contribute to increased volatility in the months ahead.

What did come from the dot plots is that the Fed is concerned with the current level of inflation and several committee members penciled in interest rate hikes.

"This Committee Will Deliver Price Stability"

Chair Warsh struck a confident tone on the Fed's core mandate. "This Committee will deliver price stability," he stated. He described current policy as maintaining ample reserves in the banking system, though he noted that reserve flows remain "uneven." For example, he said policy is still restrictive for the housing market, where elevated mortgage rates continue to weigh on affordability and activity. However, he highlighted productivity gains and business capital spending (capex), both of which look solid.

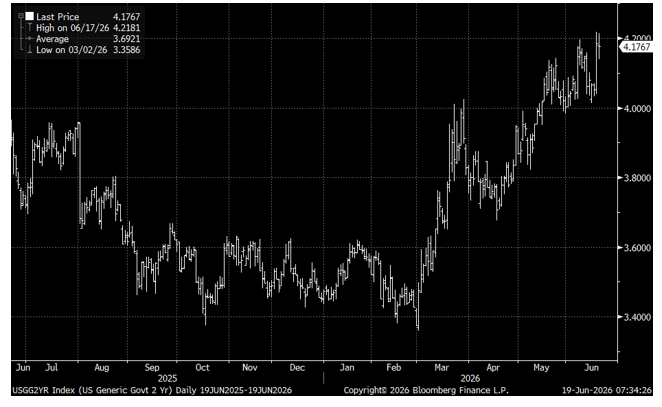

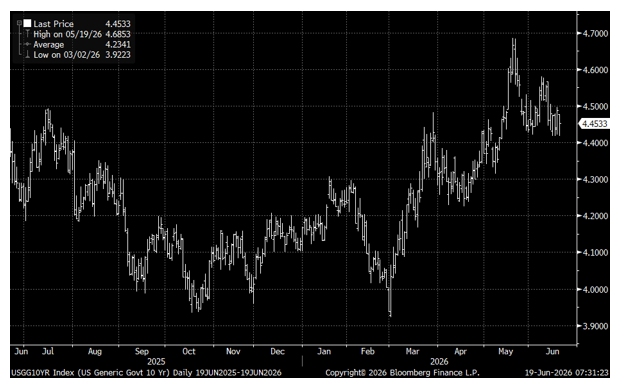

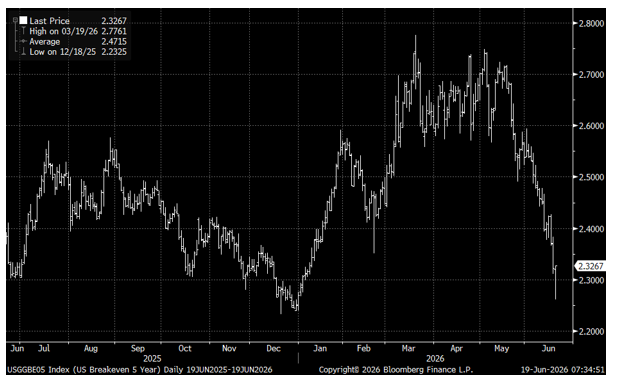

With the dot plot showing several Fed Governors projecting rate hikes this year and Chair Warsh emphasizing the Fed's commitment to price stability, the fixed income market responded by pushing the 2-year Treasury yield sharply higher. The 10-year Treasury yield initially moved modestly higher before declining the following day. The more important signal came from the Breakeven inflation market, where inflation expectations fell sharply, reflecting growing confidence in Chair Warsh's commitment to restoring price stability.

Warsh even commented in the press conference that "persistently high prices are a burden for the American people." We view this as a successful first communication with the Street.

2-YEAR TREASURY YIELD MOVES HIGHER ON WARSH'S FIRST FED PRESS CONFERENCE

10-YEAR TREASURY YIELD MOVES LOWER ON PRICE STABILITY STATEMENT

5-YEAR TREASURY BREAKEVEN YIELDS COLLAPSE AS INFLATION EXPECTATIONS FALL

Five Independent Task Forces Launched

Chair Warsh announced five new independent task forces to review key aspects of how the Fed operates. They are expected to begin delivering information this fall and aim to complete their work by year-end. The groups will examine:

- Fed communications

- The Fed's balance sheet

- Use and reliance on data sources (including new sources and better methodology)

- Productivity and jobs, specifically the pace, reach, and impact of artificial intelligence

- Inflation frameworks

Warsh stressed the need for better, more timely data. Much of the information the Fed currently relies on arrives with long delays, he noted. The delayed data is backward-looking rather than forward-looking. Warsh would like more timely data — or what we today call high-frequency data — to better determine Fed policy.

On AI, Warsh was particularly direct: "Artificial intelligence, the latest generation of general purpose technology, is perhaps as important a change in the economy and business and households that we've had in my adult lifetime. It is filled with both a huge opportunity and with risks."

Market Reaction: Hawkish Interpretation

Investors read Warsh's overall message as hawkish. The combination of a shorter, less communicative statement, the removal of forward guidance, and his focus on delivering price stability led markets to push forward expectations for the next rate hike, from December to September, and the equity markets responded by correcting on the day.

WARSH'S FIRST FOMC STATEMENT WAS PARTICULARLY TERSE

Bumpy Road to Peace in the Middle East With Oil Prices Still Falling

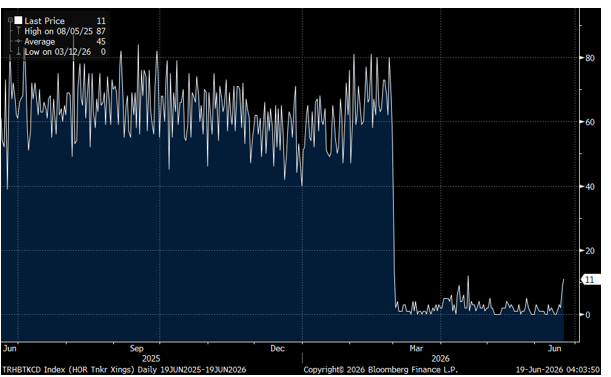

The United States and Iran signed a 14-point Memorandum of Understanding (MOU) to pause their conflict. The agreement was completed electronically — the two sides were not in the same room — and is now in effect. Oil prices that were already falling continued to fall dramatically, breaking $80 per barrel. This led to commercial shipping moving again through the Strait of Hormuz.

But this quickly changed with fighting rising between Lebanon and Israel, which led to Iran's Revolutionary Guards declaring the crucial shipping Strait closed again. The move was retaliation for what Iran and its allies view as repeated ceasefire violations by Israel in southern Lebanon. And tensions remained high as President Trump threatened Iran again.

Talks took place over the weekend in Switzerland. The U.S. and Iran concluded their first round of high-level peace talks, agreeing to a roadmap to finalize a peace deal within 60 days. The negotiations produced a communications mechanism for the Strait of Hormuz and a framework to end the conflict in Lebanon. Oil prices have been signaling — and continue to signal through their decline — that a final agreement is likely and that the Strait of Hormuz will remain open.

Late Monday morning, U.S. Treasury Secretary Scott Bessent announced that Iran has committed to free and open transit in the Strait of Hormuz and to permit IAEA inspectors into their country. As part of the framework, Treasury has issued a temporary 60-day general license authorizing the production, delivery, and sale of Iranian oil.

DAILY SHIP TRAFFIC THROUGH THE STRAIT OF HORMUZ RISING

Gulf Producers Ready to Ramp Up

Saudi Arabia says it can return to pre-war production levels in as little as two weeks. Kuwait expects to restore about 80% of its pre-war output within one week. The UAE has a bypass pipeline already in place and is also positioned to ramp back up to pre-war production levels within the next few weeks. These restarts should add meaningful supply to global markets in the coming weeks.

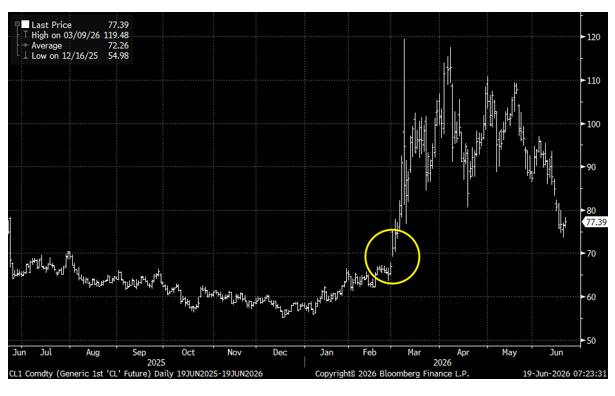

Oil Prices Collapsed Below $80

WTI crude prices have fallen below $80 per barrel on the improved supply outlook and reduced geopolitical risk. Technically, crude could decline into the low $70s and potentially test the unfilled price gap in the $67–$69 range.

WEST TEXAS INTERMEDIATE (WTI) CRUDE OIL FUTURES BELOW $80

National Gas Average Falls Below $4.00

The national average for a gallon of regular gasoline is $3.99, marking the first time prices have fallen below the $4 mark since March. This relief follows a diplomatic agreement to reopen the Strait of Hormuz and cool global crude oil prices, bringing steady relief just as the summer travel season heats up.

Consumer spending remains resilient, and lower gasoline prices should provide an additional boost to household purchasing power. According to Bank of America card data, spending rose 6% last week, while spending excluding gasoline increased 5%.

Next Steps Face Headwinds

U.S.-Iran negotiations face renewed obstacles as planned technical talks in Switzerland have been postponed due to scheduling issues and ongoing tensions between Israel and Hezbollah in Lebanon. While the 60-day window for a final agreement remains open, near-term uncertainty is likely to keep a risk premium in oil prices and regional assets despite the reopening of the Strait of Hormuz.

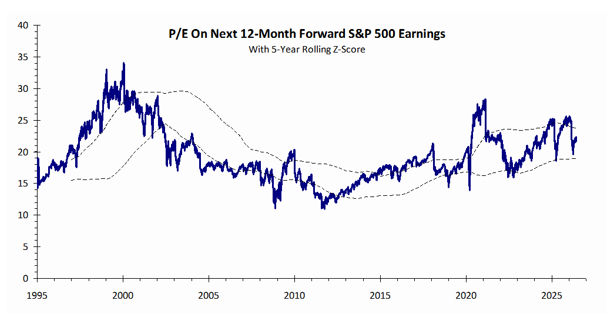

Valuations Improve Even With Higher Stock Prices

The price-to-earnings (P/E) ratio measures how expensive or cheap stocks are. The valuation of the S&P 500, as measured by its P/E ratio, has actually become more reasonable, even as stock prices have climbed higher. The primary reason is strong earnings growth, as earnings have soared 28%.

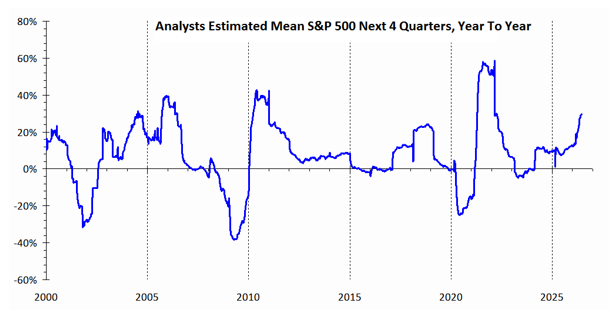

Earnings Estimates Jump Nearly 30 Percent

Wall Street analysts now expect S&P 500 companies to earn nearly 30% more over the next four quarters than they did a year ago. That sharp rise in expected profits gives investors significantly more earnings behind each dollar of stock price.

EARNINGS ESTIMATES JUMP NEARLY 30 PERCENT

Forward P/E Ratio Eases

The estimated forward price-to-earnings (P/E) ratio for the S&P 500, which compares current stock prices to expected earnings over the next four quarters, now sits just below 22 times. That is down about 3.3% from this time last year. In plain terms, investors are paying slightly less for each dollar of expected future earnings than they were a year ago.

FORWARD P/E RATIO EASES

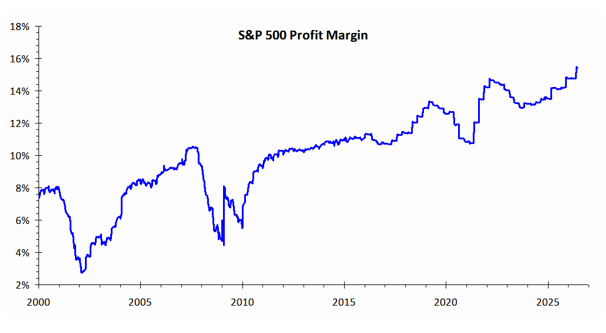

Profit Margins Hit Record High

Corporate profit margins across the S&P 500 have climbed to 15.4%, an all-time high. Profit margin is the share of every sales dollar that a company keeps as profit after expenses. Companies are keeping more of every dollar, thanks to strong productivity gains, pricing power, and efficiency improvements.

PROFIT MARGINS HIT RECORD HIGH

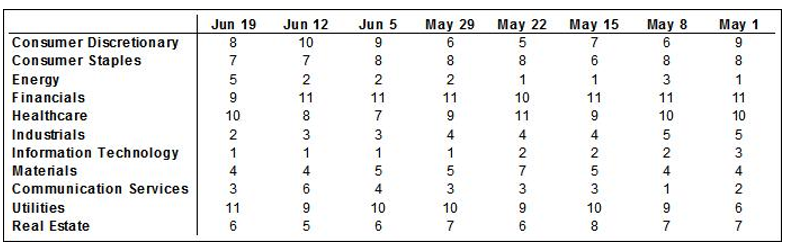

Sector Readings: Information Technology Still Strongest; Utilities Weakest

Information Technology is still in first place, followed by Industrials, then Communication Services. Utilities fall into last place this week, followed by Healthcare. Energy is no longer among the top three sectors for the first time in 28 weeks, more than half a year, showing it has entered a correction. Also, Financials are no longer one of the two weakest sectors for the first time in 19 weeks, more than a quarter, and are showing improvement; the sector has possibly bottomed.

Our sector model analyzes S&P 500 GICS sector classifications, using a weighted measure of price momentum across three time periods. We rank each sector from 1 to 11 based upon the average of its 40-, 26-, and 13-week relative price performances, with 1 being the strongest and 11 the weakest.

SECTOR RANKINGS BY 40-, 26-, AND 13-WEEK AVERAGE RELATIVE PRICE PERFORMANCE

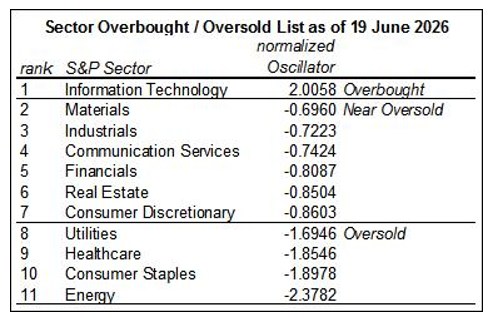

OBOS List: Information Technology Remains Unusually Overbought

Information Technology remained overbought last week, and its overbought condition is a bit extreme. Energy, Consumer Staples, Healthcare, and Utilities were oversold. The remaining sectors — Consumer Discretionary, Real Estate, Financials, Communication Services, Industrials, and Materials — were near oversold.

While not without precedence, this is an extremely rare situation. Conditions for a major sector rotation and its associated volatility are still in place with namely Technology at risk of a significant correction.

Our methodology: the overbought–oversold table measures the 13-week rate of change in the relative price of each sector, averaged over 3 weeks and normalized. Normalized oscillator values over 1.0 are considered overbought (0.6 to 1.0 near overbought); values below −1.0 are oversold (−0.6 to −1.0 near oversold). Over time, a sector tends to move back toward its normal rate of change relative to the rest of the market.

SECTOR OVERBOUGHT / OVERSOLD LIST AS OF JUNE 19, 2026

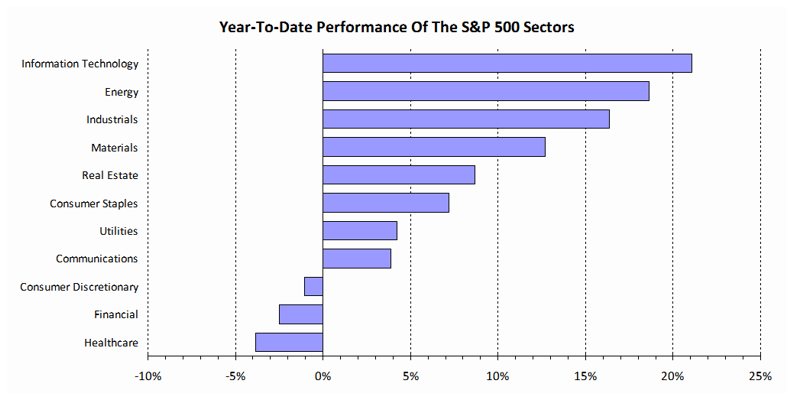

YEAR-TO-DATE PERFORMANCE OF THE S&P 500 SECTORS

Inflation, AI, Oil and the World Cup

The biggest economic headline this week arrives on Thursday, when the Bureau of Economic Analysis releases the May Core Personal Consumption Expenditures (PCE) Price Index, the Fed's preferred inflation gauge. Investors will be watching closely for confirmation of Chair Warsh's hawkish tone, particularly after he emphasized the importance of price stability in the Fed's mandate.

On the corporate side, Micron Technology (MU) reports fiscal third-quarter results after the close on Wednesday. Given Micron's strong performance and central role in the AI memory supply chain, its results and forward guidance will be closely scrutinized as a barometer for data-center spending and AI-related capital investment.

Ongoing developments surrounding oil supply restarts, traffic through the Strait of Hormuz, and the U.S.–Iran Memorandum of Understanding (MOU) will also remain in focus, as further progress — or unexpected setbacks — could influence energy prices.

Finally, we note the passing of former Federal Reserve Chair Alan Greenspan at age 100. His influence on monetary policy and financial markets spanned 18 years (1987–2006), marking a stock market boom and low employment. He served under four presidents. He will likely be remembered as one of the greatest central bankers in American history.

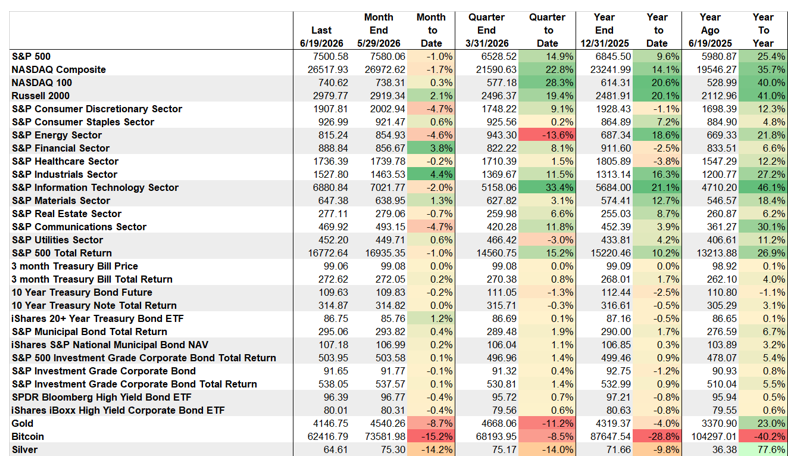

INFORMATION TECHNOLOGY WAS THE BEST PERFORMING ASSET YEAR-TO-DATE; BITCOIN STILL THE WEAKEST

The Week's Calendar

MON

No events scheduled

TUE

9:45 AMUS Flash Manufacturing PMI

9:45 AMUS Flash Services PMI

EARNINGSFedEx*

WED

10:00 AMNew Home Sales

4:00 PMFederal Reserve Board releases annual bank stress test results

EARNINGSMicron Technology

THU

8:30 AMDurable Goods

8:30 AM3rd Estimate GDP

8:30 AMWeekly Jobless Claims

11:00 AMKansas City Fed Survey

6:30 PMFRB Chicago President Austan Goolsbee speaks

FRI

8:30 AMPersonal Income, M/M%

8:30 AMConsumer Spending, M/M%

8:30 AMPCE Price Index, M/M% & Y/Y%

8:30 AMPCE Core Price Index, M/M% & Y/Y%

8:30 AMAdvance Economic Indicators Report

10:00 AMU. Michigan Final Consumer Survey

* Earnings reflect highlights. Sources: MarketWatch / Kiplinger's